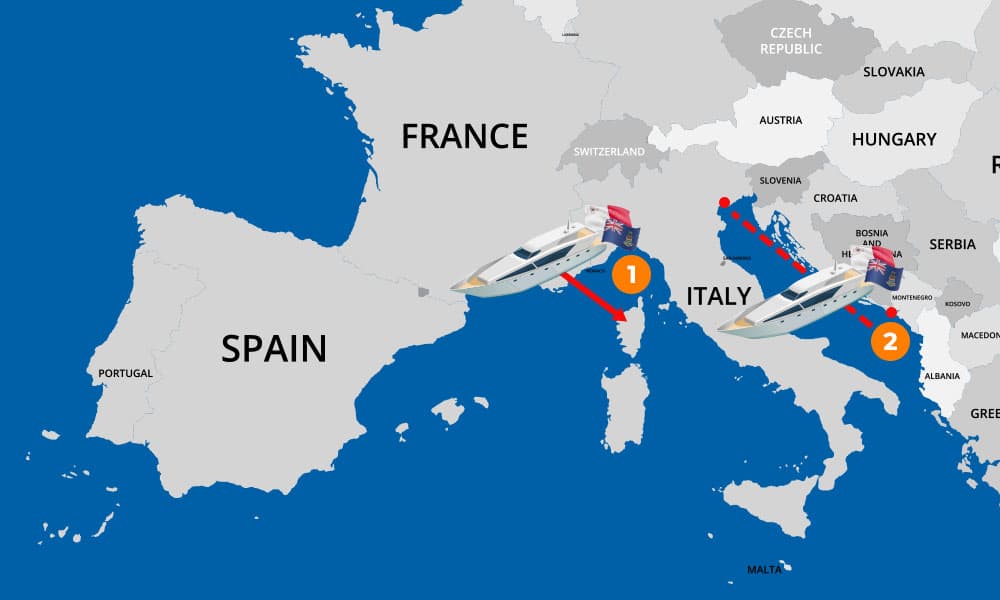

Charters from a European Union country (France) using international waters

You are a shipping company based in Malta. You organise charters from France. One of your clients is planning a stopover in Corsica. This route uses international waters (more than 12 nautical miles).This charter is subject to VAT in France. As France has opted not to tax the part of the charter located outside EU waters, you will be able to reduce your VAT bill if you can provide certain proof.

- Until 31st October 2020, charter fees were taxable in proportion to the use of the vessel in EU territorial waters. As this share became difficult to determine, the ship hiring client could apply a flat-rate reduction of 50% on the total amount of the fee, regardless of the nature of the vessel concerned.

- As of 1st November 2020, hire fees are in principle fully taxable in France. However, the part of the fee corresponding to the proportion of the actual use or operation of the vessel outside the territorial waters of the EU is exempt from VAT under Article 59a of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax. It is the taxpayer’s responsibility to assess the part of the fee that is exempt and this can be subject to inspection by the authorities. The taxpayer may corroborate the assessment by any means.

You need a tax representative to register for VAT and file your VAT returns in France with the required documents.

![]()

Charters from outside the European Union (Montenegro) using Community waters (Italy)

You are a shipowner based in Malta and are organising a charter from Montenegro. One of your clients is planning to sail in Italian waters.

As Italy has opted to tax the part of the charter located in Italy (based on the time spent in Italian waters), you will have to pay Italian VAT on this part of the charter.

You need a tax representative to register for VAT and file VAT returns in Italy with the required documents.